Balancing Legacy and Responsibility: Navigating Inheritance Decisions Amid Familial and Financial Obligations

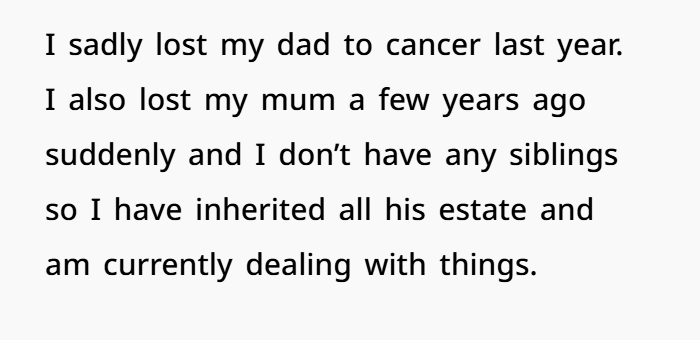

When a loved one dies, there are often a lot of feelings and responsibilities that come into play, especially when it comes to handling their estate. If you are the only child and your father died, you have to deal with a lot of different problems. Not only is she dealing with the emotional effects of losing her father, but she also has to follow his wishes, deal with money problems, and make sure her close family is safe and healthy.

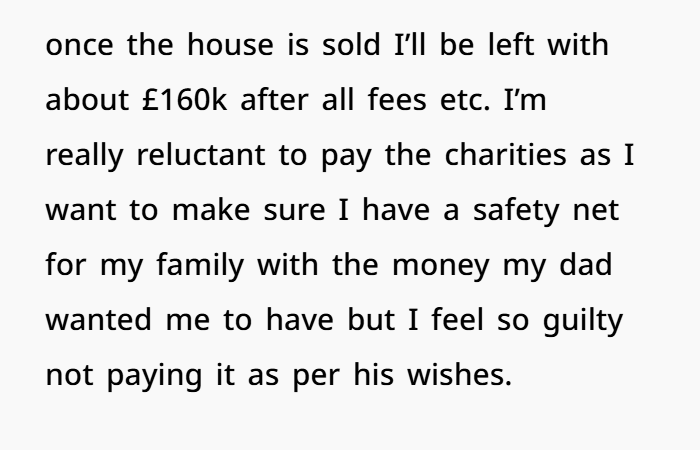

In his last few months, her father made important financial choices, like selling a valuable campervan for less than it was worth and giving more money to his siblings. He left behind a large estate that is complicated by obligations and expectations. The heir is at a crossroads. She wants to give to charities and friends as her father asked, but she also wants to make sure her toddler and family have a safe future.

This situation brings up a bigger problem that many people have when they’re planning their estate or managing an inheritance: how to balance respecting the wishes of the dead, figuring out the legal and tax issues that come up, and making smart financial decisions for their own family.

After her father had passed away, this woman didn’t even have time to grieve

Since taking care of her late dad’s estate demanded so much effort

Understanding the Legal Framework

In the UK, there are specific laws and tax rules that control inheritance issues. The Inheritance Tax (IHT), which is charged on properties worth more than £325,000, is an important factor. As an example, gifts given to people within seven years of their death may be subject to IHT. This is called the “seven-year rule.” The full 40% tax rate is applied if the person who gave the gift dies within three years of the gift. This rate drops, though, for gifts given three to seven years before death.

If the father gave £60,000 to his siblings right before he died, it might have had an effect on his inheritance tax (IHT), based on when he died and how much money he left behind. It is important for heirs to talk to financial or law experts to find out what taxes they might have to pay and make sure they follow HM Revenue & Customs (HMRC) rules.

Balancing Familial Obligations and Personal Financial Security

It can be hard to balance the personal need to honour a parent’s wishes with the need to save money. As per her father’s informal wishes, the child is thinking about giving more gifts to her father’s siblings and giving money to charities and friends. But because the estate doesn’t have a lot of money and her family needs help right away, it’s important to put financial safety first.

Before making big gifts or presents, financial planners often say to start an emergency fund, make sure you have enough insurance, and plan for future costs like college and retirement. Budgeting apps and meetings with financial planners can help you make a long-term plan for your money that combines being generous and being responsible.

The Role of Communication and Transparency

Talking to your family members openly can clear up any confusion and make sure everyone knows what to expect. Talking about the facts of the estate, such as formal duties and personal financial limits, can help people understand each other and avoid future disagreements. It’s also a chance to talk about choices about giving to charity or not being able to achieve some informal wishes because of money issues.

Charitable Donations and Tax Implications

It’s important to remember that charitable gifts can be tax-deductible, even though the father’s casual wishes included giving money to certain causes. If you give to approved charities, you don’t have to pay IHT on them, and if you leave at least 10% of your estate to charity, the IHT rate on the rest of your estate can drop from 40% to 36%. But these perks usually only apply when the donations are written into the will. If someone has private wishes that aren’t written down in a will, carrying them out might not help with taxes and could put a strain on the estate’s funds.

People who read what the woman was going through didn’t want her to give up more than she should

Finding your way through the complicated world of inheritance means balancing respecting the wishes of the dead, knowing your legal duties, and making sure your own financial well-being. Even though it’s very tempting to give a loved one everything they want, it’s important to make decisions based on good legal advice and smart financial planning. To handle a legacy in a caring and responsible way, it’s important to be honest with others, get professional help, and have a good idea of your financial situation.